Call to Action :April 14, 2026 - Property Taxes and UAB

CALL TO ACTION

Property Taxes and Unspent Authorized Budget (UAB)

April 14, 2026

Download the Printable Version of this UEN Call to Action

Call to Action: Urge Legislators to support school board plans, including goals for Unspent Authorized Budget (UAB – or carry-forward spending authority) and annual review of those plans, but oppose the arbitrary 35% limitation on UAB. The limit defies local control, and one size does not fit all.

Recent Actions: All three property tax plans (Governor HSB 563/ SSB 3034, Senate SF 2472, and House HF 2745) now include both provisions: 1) school board policy on UAB goals and maximums, with annual review, which we support and 2) mandatory limit on UAB of 35% of expenditures in the year preceding the base year, so for FY 2027 budget, it would limit to 35% of FY 2025 general fund expenditures, which we oppose. The UAB limit is effective July 1, 2026. There are 158 school districts above the proposed limit that would lose UAB, for a total reduction of $362 million statewide.

Background: Unspent Authorized Budget (UAB) is the amount of spending authority left over at the end of the fiscal year, carried forward into the next fiscal year. There are penalties for negative UAB, including: School Budget Review Committee (SBRC) workout plan, forced expenditure reductions, and a focus away from student learning as the district works to right the ship. Phase II Accreditation has closed districts with negative UAB. These severe penalties encourage districts to budget conservatively and require them to consider budget risk. UAB increased after the pandemic, driven by federal funding and unfilled vacancies. It will come down, especially with mandatory board policies on UAB, SBRC's attention to those policies, declining enrollment, continued low SSA (0-2%), and mandated salary minimums.

Talking Points:

- This restriction is an affront to local control. The Legislature would not approve if the federal government limited state carry-forward balances due to conservative budgeting practices. The State should not impose these restrictions on local school districts.

- UAB is also higher in: 1) districts with conservative budget principals, 2) districts that are property tax averse and do not have the cash reserve to back it, and 3) growing districts that save up to be able to provide new staff to open a building.

- This $325 million defunding of school districts is unnecessary; with continued low (0-2%) SSA likely and declining enrollment, UAB comes down anyway.

- The proposed 35% limitation in this Session’s Property Tax Proposals will accelerate the UAB decline, force districts to use it or lose it (the limit is higher if the district spends more in the base year), and require more cash reserves (which are replenished with property taxes).

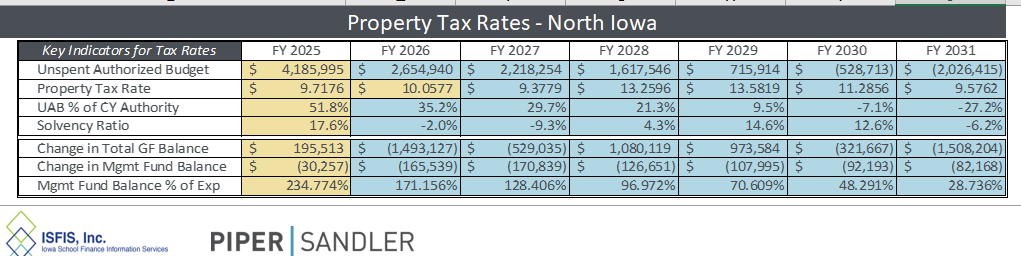

We encourage school leaders to show legislators your district’s 5-year projections, including low SSA, continued enrollment trends, and the 35% limits. Here is a real district example showing the quick impact: See the solvency ratio or cash drop, property taxes go up and spending authority UAB goes down.

Advocacy Actions: Contact your legislators today (both Senators and Representatives). Urge Legislators to support school board plans, including goals for Unspent Authorized Budget (UAB), including an annual review of those plans, but oppose the arbitrary 35% limitation on UAB. The limit defies local control and one size does not fit all.

- Find your Representatives here: https://www.legis.iowa.gov/legislators/house

- Find your Senators here: https://www.legis.iowa.gov/legislators/senate

- Please let us know if you receive any commitments of support back from your local legislators.

Thank you for your advocacy on behalf of the students and families in your school district!